Borrowing

Overview

Articles

Understanding the Key Factors of a Good Credit Score and Its Importance

Understanding the factors that contribute to a good credit score and why it is essential is paramount for financial well-being.

Are you getting the most out of your credit card? These tips can help enjoy the perks while avoiding hefty interest charges.

A line of credit acts as a preset borrowing limit. It provides you with the flexibility to access extra money quickly when you need it.

Frequently Asked Questions

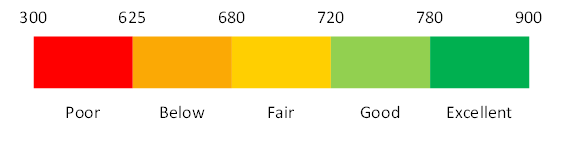

There are several types of credit scores available. Typically, the higher the score the better. A higher credit score makes it easier to qualify for loans and credit cards, often with more favorable terms, such as lower interest rates. Monitoring your credit score is important for financial planning and managing your overall credit health.

You may also need...

How can we help?

Your financial well-being comes first

Welcome to a better way to bank. Our knowledgeable team puts your financial well-being first with good, caring and transparent advice while offering all the products and services you need.

Stay in touch. Be the first to know about news, promotions and announcements. Sign up now!